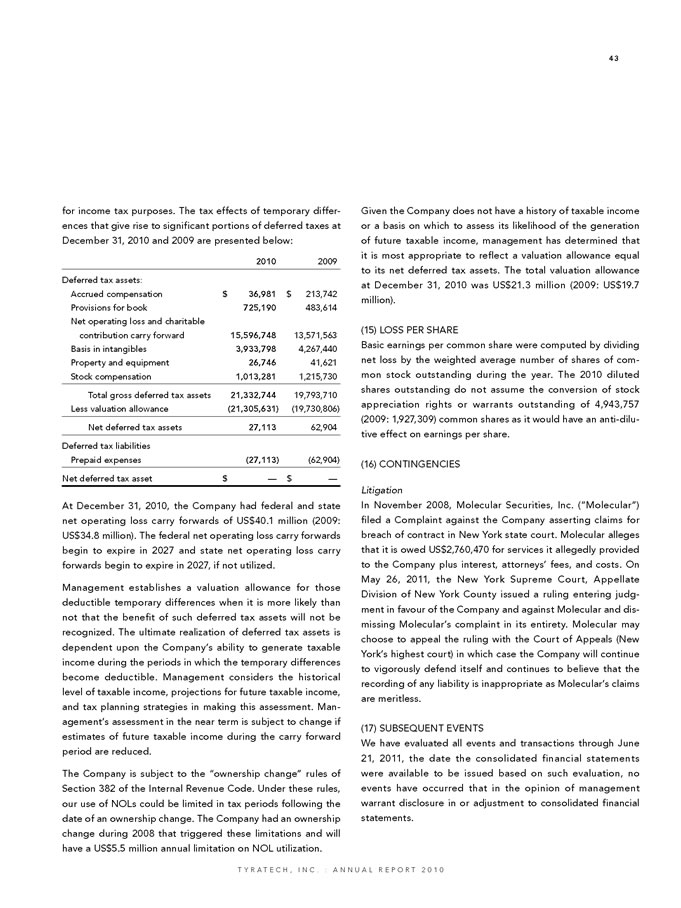

for income tax purposes. The tax effects of temporary differences

that give rise to significant portions of deferred taxes at

December 31, 2010 and 2009 are presented below:

2010 2009

Deferred tax assets:

A ccrued compensation $ 36,981 $ 213,742

Provisions for book 725,190 483,614

N et operating loss and charitable

contribution carry forward 15,596,748 13,571,563

Basis in intangibles 3,933,798 4,267,440

Property and equipment 26,746 41,621

S tock compensation 1,013,281 1,215,730

Total gross deferred tax assets 21,332,744 19,793,710

L ess valuation allowance (21,305,631) (19,730,806)

N et deferred tax assets 27,113 62,904

Deferred tax liabilities

Prepaid expenses (27,113) (62,904)

Net deferred tax asset $ - $ -

At December 31, 2010, the Company had federal and state

net operating loss carry forwards of US $40.1 million (2009:

US $34.8 million). The federal net operating loss carry forwards

begin to expire in 2027 and state net operating loss carry

forwards begin to expire in 2027, if not utilized.

Management establishes a valuation allowance for those

deductible temporary differences when it is more likely than

not that the benefit of such deferred tax assets will not be

recognized. The ultimate realization of deferred tax assets is

dependent upon the Company's ability to generate taxable

income during the periods in which the temporary differences

become deductible. Management considers the historical

level of taxable income, projections for future taxable income,

and tax planning strategies in making this assessment. Management's

assessment in the near term is subject to change if

estimates of future taxable income during the carry forward

period are reduced.

The Company is subject to the "ownership change" rules of

Section 382 of the Internal Revenue Code. Under these rules,

our use of NOL s could be limited in tax periods following the

date of an ownership change. The Company had an ownership

change during 2008 that triggered these limitations and will

have a US $5.5 million annual limitation on NOL utilization.

Given the Company does not have a history of taxable income

or a basis on which to assess its likelihood of the generation

of future taxable income, management has determined that

it is most appropriate to reflect a valuation allowance equal

to its net deferred tax assets. The total valuation allowance

at December 31, 2010 was US $21.3 million (2009: US $19.7

million).

(15) Loss Per Share

Basic earnings per common share were computed by dividing

net loss by the weighted average number of shares of common

stock outstanding during the year. The 2010 diluted

shares outstanding do not assume the conversion of stock

appreciation rights or warrants outstanding of 4,943,757

(2009: 1,927,309) common shares as it would have an anti-dilutive

effect on earnings per share.

(16) Conti ngencies

Litigation

In November 2008, Molecular Securities, Inc. ("Molecular")

filed a Complaint against the Company asserting claims for

breach of contract in New York state court. Molecular alleges

that it is owed US $2,760,470 for services it allegedly provided

to the Company plus interest, attorneys' fees, and costs. On

May 26, 2011, the New York Supreme Court, Appellate

Division of New York County issued a ruling entering judgment

in favour of the Company and against Molecular and dismissing

Molecular's complaint in its entirety. Molecular may

choose to appeal the ruling with the Court of Appeals (New

York's highest court) in which case the Company will continue

to vigorously defend itself and continues to believe that the

recording of any liability is inappropriate as Molecular's claims

are meritless.

(17) Subsequent Events

We have evaluated all events and transactions through June

21, 2011, the date the consolidated financial statements

were available to be issued based on such evaluation, no

events have occurred that in the opinion of management

warrant disclosure in or adjustment to consolidated financial

statements.

43

T y r a T e c h , I n c . : A n n u a l R e p o rt 2 0 1 0